Seeing a renewal notice with a Greensboro car insurance increase can be jarring, especially when your driving habits haven’t changed. In many cases, the rise reflects broader claim costs and rule changes in North Carolina rather than something you did.

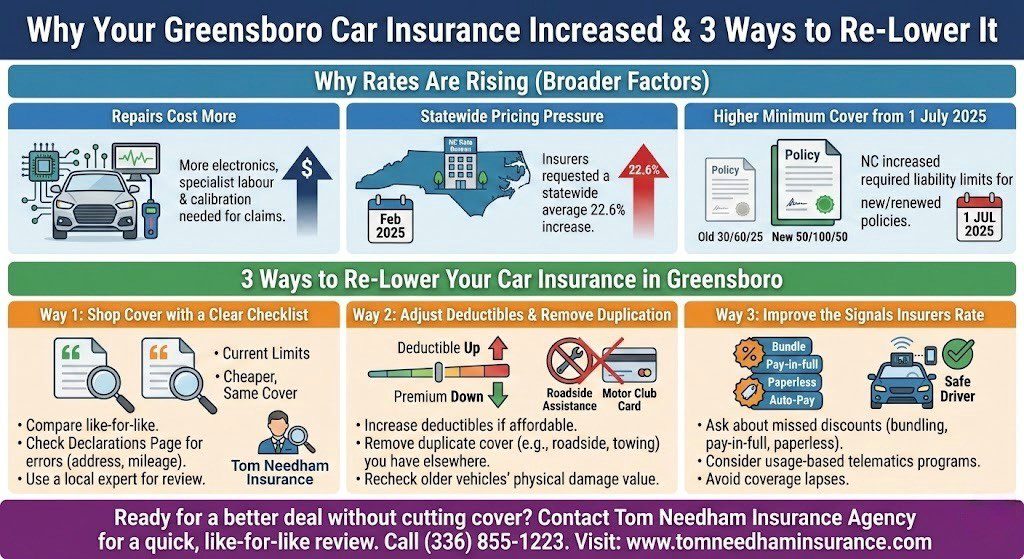

Why rates are rising

1. Repairs cost more

Cars now carry more electronics, and repairs often require specialist labor and calibration. When each claim costs more to settle, premiums tend to follow.

2. Statewide pricing pressure

North Carolina sets many private passenger auto rates through a formal process. The North Carolina Rate Bureau can file for a statewide average change and the North Carolina Department of Insurance reviews it.

In February 2025, insurers requested a statewide average 22.6% increase, showing the scale of cost pressure they reported across the market.

3. Higher minimum cover from 1 July 2025

For policies new or renewed on or after 1 July 2025, North Carolina increased minimum liability limits to 50/100/50 from 30/60/25. More required cover can lift the price at renewal even if nothing else changes. Other 2025 updates also affected how some surcharges and lookback periods work for certain drivers.

How to Re-lower Your Car Insurance in Greensboro

Way 1: Shop your cover with a clear checklist

Compare like with like

Pull out your declarations page and confirm the basics: garaging address, annual miles, vehicle trim, and listed drivers. Small errors are common and they cost real money.

Request a few quotes that match your current limits and deductibles. If a cheaper quote drops cover, it isn’t a fair comparison.

Use a local set of eyes

A quick review with experts such as Tom Needham Insurance can help you spot rating issues and check whether another insurer prices your profile more favorably.

Way 2: Adjust deductibles and remove duplication

Increase deductibles only if you can pay them

Higher comprehensive and collision deductibles often reduce premiums. Keep the figure at a level you could pay tomorrow without stress.

Cut double-ups, not protection

Roadside assistance, towing, and rental cover are handy, but they may overlap with a motoring club, credit card, or manufacturer plan. Remove what you already have elsewhere.

Recheck cover on older vehicles

If your car’s value is modest, full physical damage cover can become poor value. Balance the annual premium against what the car is realistically worth, then decide with your budget in mind.

Way 3: Improve the signals insurers rate

Ask about overlooked savings

Car insurance discounts Greensboro drivers often miss include multi-policy bundling, pay-in-full, paperless billing, and automatic payments. These can lower the bill without weakening your core cover.

Consider usage-based programs if they suit you

Telematics can reward calm, consistent driving. Read the terms so you know what’s tracked and how it affects renewals.

Avoid lapses if the car stays registered

North Carolina requires continuous liability insurance for registered vehicles, and out-of-state policies aren’t accepted for NC registration. If you need to stop driving, deal with plates and registration before cancelling cover.

Ready to see whether you can get a better deal without cutting cover? Contact Tom Needham Insurance Agency for a quick policy review or a like-for-like quote comparison at (336) 855-1223.

Frequently Asked Questions:

- Why did my car insurance go up in Greensboro with no accidents?

Premiums can rise when claim costs increase in your area, even if your record is clean. Repair and maintenance costs have climbed, partly because vehicles are more complex to fix. Pricing can also reflect local claim frequency, theft trends, and broader statewide rate pressure. Ask your insurer which factor changed at renewal.

- How can I lower my car insurance in Greensboro quickly?

Check your policy details first: mileage, garaging address, drivers, and vehicle trim. Then get two or three like-for-like quotes with the same limits. If you have savings to cover it, a modest deductible increase can help. Finish by removing duplicated extras such as towing or rental cover, and ask about payment and bundling discounts.

- What is the minimum car insurance required in North Carolina now?

For policies new or renewed on or after 1 July 2025, minimum liability limits increased to 50/100/50. That means more built-in protection than the old 30/60/25 minimums, which can raise premiums at renewal. If you carry higher limits already, the legal change may have less impact.

- Does raising my deductible lower my premium?

Often, yes. A higher deductible reduces what the insurer expects to pay on smaller claims. The trade-off is that you pay more out of pocket after an accident. It can help to set the deductible at an amount you could pay from an emergency fund, not from a credit card.

- How often should I shop around for car insurance?

A yearly check at renewal is sensible, and it’s also worth shopping after moving, changing vehicles, or adding a driver. Keep your cover levels steady while comparing so you can see the real difference in price. Even if you stay put, you may gain leverage to negotiate a better rate.