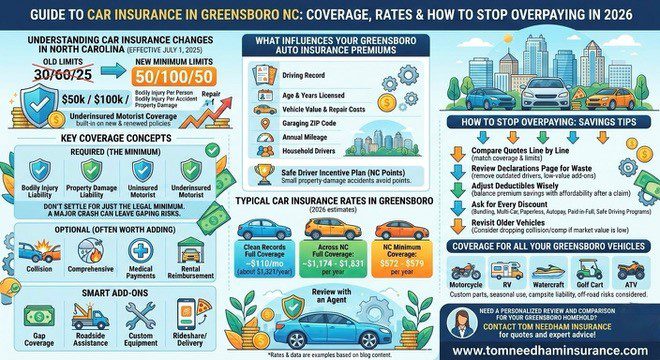

Shopping for car insurance in Greensboro NC is harder than it looks. A low premium can hide weak protection, while a higher quote may include coverage you do not need. In 2026, Greensboro drivers face another layer of complexity because North Carolina’s rules changed for policies written or renewed on or after July 1, 2025. Minimum liability limits are now higher, and underinsured motorist coverage is built into new and renewed policies. That means many drivers are paying more than they did a year ago, even without an accident.

What Greensboro drivers should know before buying insurance

- Quotes are built on more than your car. Insurers look at your garaging ZIP code, driving record, annual mileage, household drivers, prior coverage, and the vehicle itself. The same carrier can price two Greensboro households very differently.

- Price only matters when the coverage matches. Comparing a bare-bones policy to one with collision, comprehensive, rental reimbursement, and higher liability limits is not a fair test.

- North Carolina requires continuous liability coverage on registered vehicles. If a car is registered in the state, it cannot sit uninsured just because it is not being driven much. That rule catches people off guard.

- “Full coverage” is a nickname, not a legal category. Most people use it to mean liability plus collision and comprehensive, but exact features vary by policy.

Car insurance coverage in Greensboro, NC: What you need and what’s optional

Start with the minimum coverage the law requires, then choose extra protection based on your budget and how much risk you want to take. In North Carolina, drivers now need higher liability limits, plus uninsured and underinsured motorist coverage on new or renewed policies.

Starting July 1, 2025, the minimum limits increased from 30/60/25 ($30,000 for injuries to one person, $60,000 for injuries per accident, and $25,000 for property damage) to 50/100/50 ($50,000 for injuries to one person, $100,000 for injuries per accident, and $50,000 for property damage.)

- Usually required

- Bodily injury liability: pays when you injure someone else.

- Property damage liability: pays for damage you cause to another person’s vehicle or property.

- Uninsured motorist coverage: helps when the at-fault driver has no insurance.

- Underinsured motorist coverage: now included on new and renewed policies under the 2025 change.

- Often worth adding

- Collision coverage for damage to your own car after a crash.

- Comprehensive coverage for theft, hail, fire, vandalism, falling objects, and similar losses.

- Medical payments coverage for certain injury costs regardless of fault.

- Rental reimbursement or transportation expense coverage if you would need a car while yours is in the shop.

- Sometimes optional, but smart for certain drivers

- Gap coverage for financed or leased cars.

- Roadside assistance if you do not already get it elsewhere.

- Custom equipment coverage for upgraded wheels, audio systems, or other add-ons.

- Rideshare or delivery coverage if you drive for an app-based service. NC DOI advises drivers to review this exposure with an agent because a personal auto policy may not be enough.

A common mistake is buying only the minimum because it satisfies the law. That may work on paper, yet it can leave a serious gap after a major crash, especially with today’s repair and medical costs.

Car insurance rates in Greensboro, NC: What people are paying in 2026

In Greensboro, some drivers with clean records may find full coverage for around $110 per month, or about $1,321 per year.

Across North Carolina, average premiums for full coverage are often estimated between about $1,174 and $1,831 per year, while minimum coverage may fall between roughly $572 and $579 per year.

Your actual rate will depend on factors such as your driving history, age, vehicle, coverage choices, deductible, and where you live.

- Why rates vary so much

- Age and years licensed

- Tickets, accidents, or DUI history

- Vehicle value and repair cost

- Coverage level and deductible choice

- Rating factors tied to your profile and location

- Why 2026 feels more expensive

- Repair costs remain elevated.

- North Carolina approved an average 5% auto rate increase beginning October 1, 2025, after a settlement.

- Higher required limits from 2025 pushed many renewals upward.

Drivers looking for auto insurance in Greensboro NC should keep one more point in mind: violations can trigger surcharges under North Carolina’s Safe Driver Incentive Plan, though some lower-level speeding violations and small property-damage accidents may avoid points if the rules are met.

How to stop overpaying for car insurance in Greensboro

- Compare quotes line by line. Match liability limits, deductibles, collision, comprehensive, and extras before deciding which policy is cheaper.

- Review your declarations page for waste. Duplicate roadside coverage, low-value add-ons, or outdated driver information can quietly raise the bill.

- Adjust deductibles with care. A higher deductible can lower premiums, but only if you could comfortably pay that amount after a claim.

- Ask for every discount you legitimately qualify for. Bundling, multi-car, paperless billing, autopay, paid-in-full options, and safe driving programs can all help. Consumer reporting also shows many shoppers save money when they switch carriers after comparing comparable policies.

- Revisit older vehicles. If a car’s market value has dropped sharply, paying for both collision and comprehensive may no longer make sense.

The best savings move is not chasing the lowest number. It is matching coverage to how you actually drive, then trimming what no longer serves a purpose. That is where a local policy review often pays off.

Car insurance for every Greensboro driver

Auto insurance needs can vary widely across Greensboro households, especially when coverage extends beyond a standard car. A smart policy review should account for how each vehicle is used and the risks that come with it.

- Motorcycle insurance: Helps cover liability, bike damage, theft, and rider-related expenses. Custom parts and seasonal use may also affect coverage needs.

- RV insurance: May include protection for driving risks, campsite liability, personal belongings, and emergency travel expenses, depending on how often the RV is used.

- Watercraft insurance: Can cover boat or jet ski damage, liability, theft, trailers, and onboard equipment. Storage and seasonal use matter.

- Golf cart insurance: Useful for carts driven in neighborhoods, private communities, or recreational areas where liability and theft risks still apply.

- ATV insurance: Often covers collisions, overturns, theft, liability, and custom equipment, especially for off-road use.

Get the coverage that fits your car, motorcycle, RV, watercraft, golf cart, or ATV without paying for protection you do not need. Contact Tom Needham Insurance for a personalized review and compare options built for Greensboro drivers.

Frequently Asked Questions:

1) What is the minimum car insurance required in North Carolina in 2026?

North Carolina requires liability insurance, uninsured motorist coverage, and, for policies written or renewed on or after July 1, 2025, underinsured motorist coverage. The current minimum liability limits are 50/100/50, meaning $50,000 per person, $100,000 per accident for bodily injury, and $50,000 for property damage.

2) Is full coverage required in Greensboro?

No. The law requires the state minimum coverages, not “full coverage.” People usually use that term to describe liability plus collision and comprehensive. Lenders may require broader protection on financed or leased cars, which is different from a state legal requirement.

3) Why did my premium go up if I did not file a claim?

Your rate can rise because of statewide approved increases, costlier repairs, higher medical costs, or a move to the new minimum limits. A clean record helps, but it does not shield you from market-wide pricing changes.

4) What is the difference between liability and collision coverage?

Liability pays for injuries or property damage you cause to others. Collision pays for damage to your own vehicle after a crash, subject to your deductible. One protects your legal responsibility; the other protects your car.

5) How can I lower my rate without cutting needed protection?

Start by comparing equal quotes, checking for outdated drivers or duplicate extras, and asking about discounts. Then review deductibles and whether older cars still need collision or comprehensive. A local agency like Tom Needham Insurance Agency can spot gaps and excess spending faster than a quick online quote form.

About: Tom Needham Insurance Agency is an independent Greensboro agency that helps individuals and businesses compare coverage options across auto, home, business, and life insurance while shopping multiple carriers for value and fit. The agency emphasizes local service, clear guidance, and personalized support so clients can choose protection that matches their needs and budget.