A renewal notice lands in the mailbox. The premium ticked up again. Most people glance at the new number, sigh, and pay it. That sigh is where the money goes.

Insurers rarely call to tell you about a discount you just became eligible for. Your kid made the honor roll. You paid off the car. You started working from home and stopped commuting. Each of those can lower a premium, and none of them does it on its own. The credit sits there, unclaimed, until somebody asks. Most of the car insurance discounts below work exactly that way. Here are the ten that North Carolina drivers miss most.

For a broader look at coverage options, local rates, and additional ways to reduce your premium, read our complete guide to car insurance in Greensboro, NC.

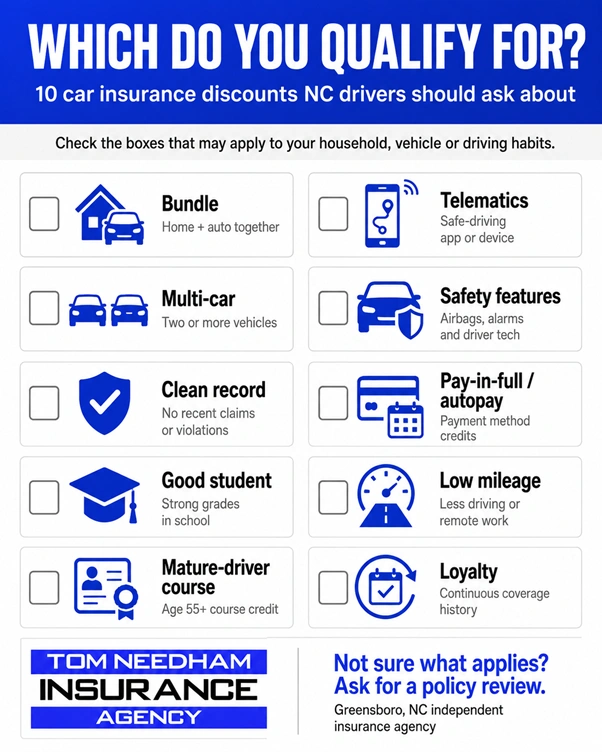

1. Bundle your home and auto

The biggest single discount for most households is also the easiest. Put your car and homeowners or renters policy with the same insurer, and both usually drop. The carrier would rather hold all your business than half of it, so it pays for the privilege. Families already carrying auto insurance coverage and a separate home policy often find this is the fastest cut available. Ask what the bundled number looks like before you assume your current split is cheaper.

2. Insure more than one car

Two or more vehicles on the same policy almost always cost less per car than two standalone policies. Same logic as bundling: the insurer locks in more of your business. This trips up couples who kept separate policies from before they lived together, and households where a teenager’s car ends up on its own plan. Folding everything under one policy is usually cheaper, even after the teen driver gets added in.

3. Keep a clean record, and know how NC rewards it

North Carolina ties safe driving to your wallet directly. The state’s Safe Driver Incentive Plan was created by state law to assign points for at-fault accidents and certain convictions, and to reward drivers who stay clean. No points means no surcharge, and many insurers add their own good-driver credit on top. A few years without a claim or violation can quietly become one of the larger discounts on your policy. If you carry car insurance in Greensboro NC, a clean record is worth real dollars.

4. Good student discount

If there’s a full-time student in the house with solid grades, usually a B average or better, most carriers take money off. The reasoning is simple. Students who manage their grades tend to manage risk behind the wheel. It applies to high schoolers and college students, often up to age 25, and proof is just a report card or transcript. Plenty of parents never think to mention the honor roll to their agent, so they never see the credit.

5. Telematics and safe-driving apps

Let the insurer see how you actually drive, through a phone app or a plug-in device, and a good record earns a discount. It tracks braking, speed, time of day, and mileage. Calm drivers who avoid heavy late-night highway runs tend to come out ahead. The catch is that hard braking and high mileage can cancel the benefit out. Worth a try if you drive gently and not constantly.

6. Safety and anti-theft features

The car itself can lower the bill. Anti-lock brakes, airbags, electronic stability control, automatic emergency braking, and anti-theft systems all reduce what an insurer expects to pay out, so they hand some of that back. Newer vehicles often qualify automatically. Older ones with aftermarket alarms or trackers may need you to point them out. When you switch cars, confirm which features are on file. The discount only applies if the insurer knows about them.

7. Pay in full, on autopay, paperless

How you pay can shave off a few percent. Paying the full six-month premium up front usually beats monthly installments, which often carry small service fees. Setting up automatic payments tends to add a credit, and so does going paperless. None of these are large on their own. Stacked together, on a policy you are paying for anyway, they add up to real money across a year.

8. Low-mileage and pay-per-mile

Drive less, pay less. If you retired, shifted to working from home, or simply do not rack up many miles, you may be paying for a commute you no longer make. Some insurers offer a low-mileage discount. Others sell pay-per-mile policies built around exactly how far you go. Anyone covering well under the average annual mileage should ask whether their rate still fits their real driving, then request an updated auto insurance quote in Greensboro.

9. Loyalty and tenure

Staying put can pay, up to a point. Some carriers reward years of continuous coverage with a loyalty credit, and a long claim-free history strengthens your standing. Here is the caveat. Loyalty is not the same as the best price. The discount is real, but it earns its keep only when you check it against fresh quotes now and then.

Why an agent finds what you cannot

Here is the part that trips people up. A captive agent, the kind tied to a single national brand, can only offer that one company’s discounts. If their carrier does not reward low mileage, or does not count your safety package, you never hear about it. An independent agency works the other way around. As a Greensboro insurance agency representing more than a dozen carriers, we line your situation up against each company’s rules and surface the credits that actually apply. The Greensboro insurance agents on our team run that comparison every day, which is how the missed savings come to light.

Let’s find the money you’re leaving behind

At Tom Needham Insurance Agency, hunting down these credits is the whole job. Tell us about your cars, your home, your drivers, and your habits, and we will compare top-rated carriers to see which discounts you genuinely qualify for. It costs nothing to look, and there is nothing to lose but the overpayment. Request your free insurance quote today, and let us put that money back where it belongs.

Disclaimer:

Discounts, eligibility rules and savings vary by insurance carrier, policy, driver profile, vehicle, coverage selection and North Carolina filing rules. Not every discount listed here is available from every insurer or for every driver. Some programs may be limited, unavailable or applied only to certain coverages. The best way to confirm available savings is to review your policy with a licensed North Carolina insurance agent.